TORONTO - Within months, Canadian shoppers could have the option of paying for

purchases with cash, credit or by BlackBerry.

Whether they'll actually do so is another matter.

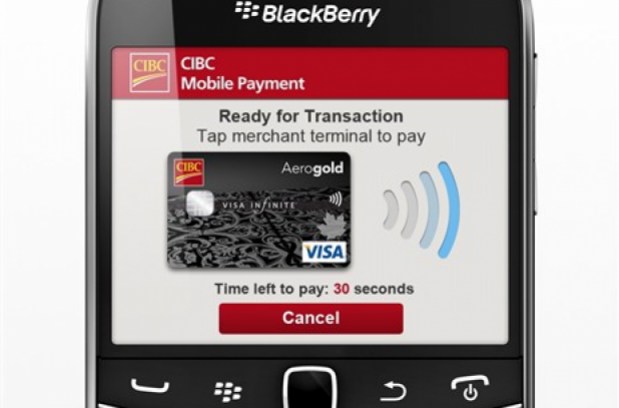

CIBC (TSX:CM) and Rogers Communications (TSX:RCI.B) announced a partnership

Tuesday that will harness the Near Field Communication technology built into

newer BlackBerrys, allowing the phones to act like a credit card at

checkout.

The technology will work exclusively with CIBC credit card accounts and

BlackBerrys on the Rogers network at launch, which is tentatively scheduled for

"later this year."

"Some people might not carry a wallet but they'll always have their

smartphone," said David Williamson, senior executive vice president of retail

and business banking for CIBC.

But consumer surveys suggest Canadians may not be all that keen on the notion

of a digital wallet.

New research released Tuesday by Google suggested Canadians are lukewarm on

the idea of using their phones to make online purchases. After speaking with

1,000 Canadian smartphone users, only 20 per cent said they had made a mobile

purchase and only 16 per cent said they expected to boost their mobile shopping

in the following year.

Meanwhile, a Mastercard research project called the Mobile Payments Readiness

Index ranked Canada as the second-best of 34 global markets in terms of being

set to embrace mobile transactions (Singapore ranked first).

But while Canada ranked high for its partnerships between banks and

governments, and its business and regulatory environments, it was below average

when it came to the consumer readiness metric.

Mastercard estimated only about 15 per cent of Canadian consumers were

willing to use a mobile phone to pay in stores, which was two percentage points

below the global average.

But Ian Shelley, a partner at KPMG, believes that figure is probably

low-balling Canadian interest in the technology, which is sure to grow as word

about it spreads.

"The 15 per cent number is really just the tech-savvy individuals who have

kept up with the mobile payments agenda," said Shelley.

"But once these sorts of announcements come up I think you'll see much

greater adoption."

Adam Chow, 20, said the only thing holding him back from trying out the

technology is his choice of phone, Apple's iPhone. While CIBC said it would

eventually make other phones compatible with its mobile payment system, probably

starting with Google Android models, the latest iPhone doesn't support NFC.

Chow could imagine wanting to pay with his phone, since he'd probably have it

in his hand anyway while waiting in line.

"It's quick, right, you have your phone in your hand, just wave it and the

purchase is done."

But it may be more difficult to sell the technology to some consumers early

on, before the functionality is fully fleshed out," Shelley said.

"What makes this attractive for me today? Because I do have a wallet and it

works quite well," said Shelley when asked to predict consumer reaction.

But he said it probably won't be long before other banks and credit card

companies, as well as loyalty card programs, get involved.

Williamson admitted he's anxious to see that happen.

"I've got two inches of cards for car rental places, hotel loyalty cards —

this, that and everything kind of cards — so if I could put those on the phone,

I could get rid of the ridiculous number of cards I carry," he said.

"I'd be all over that."

And don't be surprised if digital government ID cards become a reality in the

not-too-distant future, Shelley added.

The final report of the Task Force for the Payments System Review, which was

commissioned by the federal government, called for a safe, secure form of

digital ID to be created.

"Propel the build of a digital identification and authentication (DIA) regime

to underpin a modernized payments system and protect Canadians' privacy," reads

a recommendation in the report, which notes that federal and provincial

governments have been proactive on digital ID talks.

"Thinking about the credentials you have in your wallet," Shelley said,

"pretty much any of them can go away."

0 comments

Post a Comment